How have we got by without an LGEN thread?

Good dividend payer, strong business, not as doglike as AV. A definite core part of my stock picks. anyone else?

How have we got by without an LGEN thread?

Good dividend payer, strong business, not as doglike as AV. A definite core part of my stock picks. anyone else?

In my top bracket when it comes to what I’ll hold “forever”

Their management from what I can see is so in touch with future trends. Massive investment into the UK’s largest electric vehicle charging stations.

And also they have a modular home facility built in what they reckon will be the long term solution to the UK’s affordable housing shortage. I was listening to a podcast with Simon Zutchi (sp) he’s the UK’s version of Grant Cardone per say and the podcast was looking at housing predictions for the next decade. And he said that the housing trend is definitely going modular, done a bit of research and lo and behold L&G are already on the ball, great company ![]()

https://www.24housing.co.uk/news/lgs-modular-factory-to-deliver-the-norths-much-needed-homes/

I’m with you here. I’m a big fan of LGEN and everything they’re doing. I’ve been toying with the idea of moving out of Aviva and adding it all to my LGEN holding. It breaks all my rules I set myself at the beginning but I see so much upside long term.

This is one I’ve been mulling over to invest in and must admit their track history does look pretty good to have as a long term keeper.

Little know L&G facts.

Founded in 1836, classified as an “insurance” company, yet only just over 10% of profits comes from insurance, dropping even further with the recent sale of their general insurance business.

Global leader in Pension Risk Transfer - 30% UK market share, 3% US market share.

10th largest investment manager in the world, with assets under management of £1.1trn - first U.K. asset manager to break £1trn mark, by some measures fastest growing one this side of the pond.

Major investments in future cities, with targeting to regenerate 15 cities in the U.K.

£1bn+ revenue from housing, the 9th largest house builder in the U.K., with a modular housing factory north of Leeds that is based on the principles of precision engineering - CEO of module housing is ex Rolls Royce. Builds retirement villages, affordable housing, rent-to-buy.

26% market share in lifetime mortgages, 18% market share in individual annuities, 3.4m workplace pension customers. Operates in 85% of the global Defined Benefits markets.

Corporate ethos is all about Inclusive Capitalism, cantering on macro economic trends of ageing demographics, globalisation of asset markets, creating real assets, welfare reforms, tech innovation and today’s capital.

2011-2015 delivered a 10% growth in EPS, on target to deliver 11% by the end of 2020, following 2020 aiming to deliver its global ambition.

I’m long LGEN. I wanted more exposure to UK (which I didn’t have at all really before 2019), and auto-enrollment will be a long term cash cow.

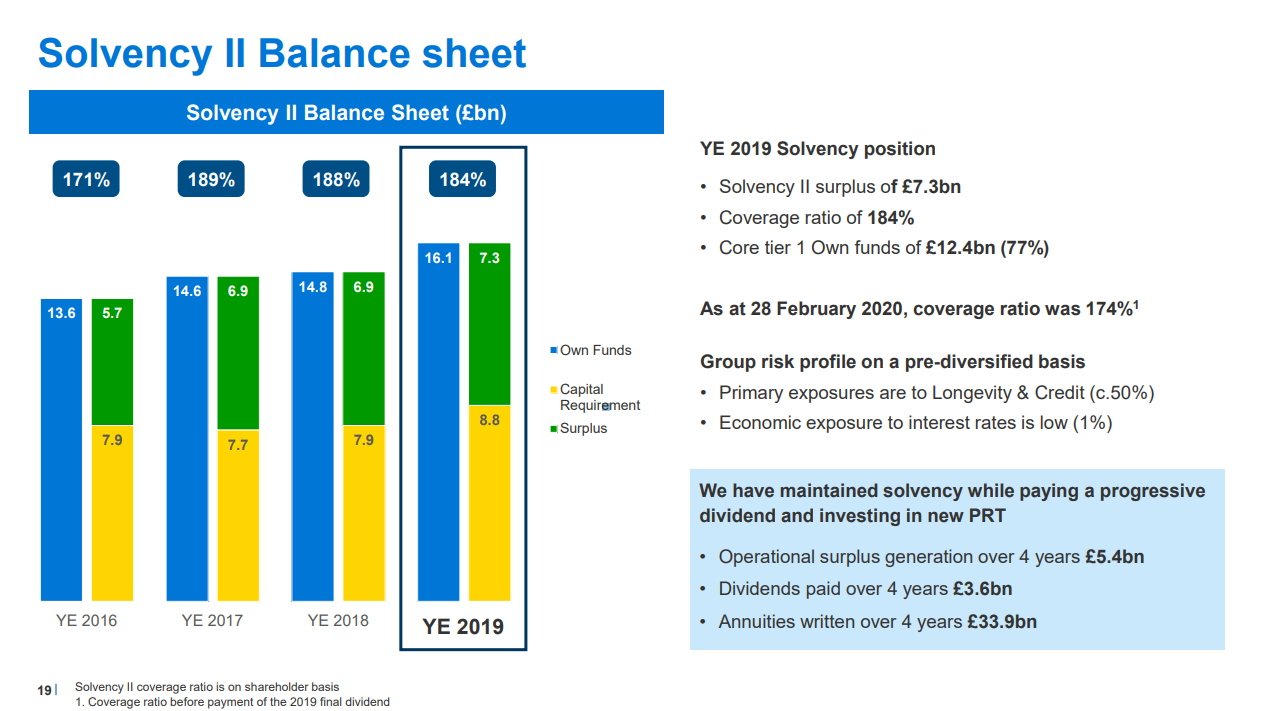

Their FY19 results came in today:

Most impressive was that for the last decade, they posted double digit year-on-year growth on four key metrics:

Breaking down operating profit by division:

They’re a great business and these results prove it.

They might be my ‘if you could only have one stock and hold it forever’ choice…

For those who like to keep tabs on your dividends you can see the ex div dates here:

And add them to your calendar.

Now 50% down from last months highs!!

P/E Ratio of just over 5.

Dividend now over 10%

Payout Ratio still 55%

Free Cash £13.3bn

And only £5.3bn of debt.

Anyone else think LGEN is massively attractive now? I’ll definitely be averaging down, got confidence they will ride this storm.

They’re an absolute steal. There’s no way they will go under as they got plenty of solvency II coverage. They’re also diversified across insurance, pension, investments and real estate - stuff people will always need.

Every large company will be in trouble then, not just L&G - at least their cash reserves are good.

Looks solid to me. If we’re worried about LGEN not having the reserves then a lot more insurers will go down with them.

I’ve a holding of L and G. Like the company, good valuation

I picked up a few shares yesterday. People will still need investments, pensions, car insurance etc

Dividend yield strong (fingers crossed sustainable)

More diversification into the portfolio

They sold general insurance division though, it’s too price sensitive and difficult to make profit - was a drag on the group. They also sold their closed book Mature Savings business, and lots of other things like CoFunds over the years, so it’s a much more streamlined group with high margin / high growth businesses.

Of these, what will most be impacted by coronavirus? LGEN is around half of what it was a few months ago, falling more than the broader market.

Life insurance payments may increase, but even if it’s at Italy levels then it’ll be a drop in the ocean compared to normal payout rates.

Investment management will be hit, as their assets under management will take a hit as the market has dropped, but so does every other asset manager. As the tenth largest in the world they’re well positioned to weather the storm, as clients are unlikely to leave to another asset manager as they’re all in the same boat.

PRT may benefit, if companies are under even more pressure, offloading their underfunded pension books may advantageous for them.

Retirement will continue in a similar vein, people still will pay on and get paid out.

Investment management i did my university placement at landg. The volume of investment at the end of the personal tax year was huge

…now a lot depends upon how much profit is generated from current customer investment or the last minute topping up to limits. Lots of 1% fees may not materialize if investors are nervous but this is small

Also capital investment depends a lot around diversification in asset class, solar seems a product you can contract future revenue streams prior to building out people need electric, where as office buildings you need tenants and growing businesses to occupy there could be risk here…

Personal investing division is a tiny fraction of their AUM. The vast majority is institutional investors like governments, pension funds, sovereign wealth funds, insurers and the likes. Most of the rest is workplace pensions, with 3.7m individual customers who pay in on a monthly basis regardless of tax year end or not. Then a small portion via distribution of funds via wealth management firms. And a roundup error on their D2C proposition, which will be reliant on year end bonus contributions.

I guess the risk is that the pensions that L&G have insured go under?