The ISA will be £3 a month and the only other fee would be if you wanted an instant trade instead of the basic free one at 4pm. That would be £1. There’s 0.5% government stamp duty on individual stocks, but not on ETFs or American stocks

There is currently no transfer in ability from over providers but they’re working on that. Freetrade won’t charge you transfer fees but you’ll need to look and see if Moneybox have a charge. There have been requests for a Freetrade LISA but it’s not on the roadmap.

There’s no ethically based at the moment but once the new investment platform is built they will be able to add loads more new stocks a lot quicker, and that’s expected in the next few months as well. That will also mean fractional shares will be available which will help you buy those expensive American stocks

Not sure if you’ve seen this blog on diversification but it’s worth a read

What’s the existing total value of your investments?

Moneybox’s standard charge seems to be £1/month + 0.45% of total, while Freetrade’s ISA accont charge is £3/month. 0.45% of £445 is £2, plus the £1 is £3. So if you have more than £445 already invested, Freetrade will be cheaper.

At these small amounts invested, you also don’t actually need an ISA, since you won’t pay any taxes for quite some time due to your personal allowances.

Which means you don’t need to wait for Freetrade to implement ISA transfers. You can just close your Moneybox account, take the cash out (losing ISA wrapper status), and put it in Freetrade’s free basic account.

Then you’re not paying anything in fees until it’s worth paying for an ISA.

You don’t have to answer that but everything @anon287192 says is spot on regarding your options.

Sorry for butting in @anon287192 its just I’m a fairly new investor too (started learning on this forum about 6 months ago) and was a bit embarrassed at my small portfolio amounts at first, and a question like this on one of my first posts might have made me nervous.

@joe For info if it helps as an example, I am well under the limit for needing an ISA and am using freetrades free general investing account with the intention of moving to an ISA when I have probably 15k+

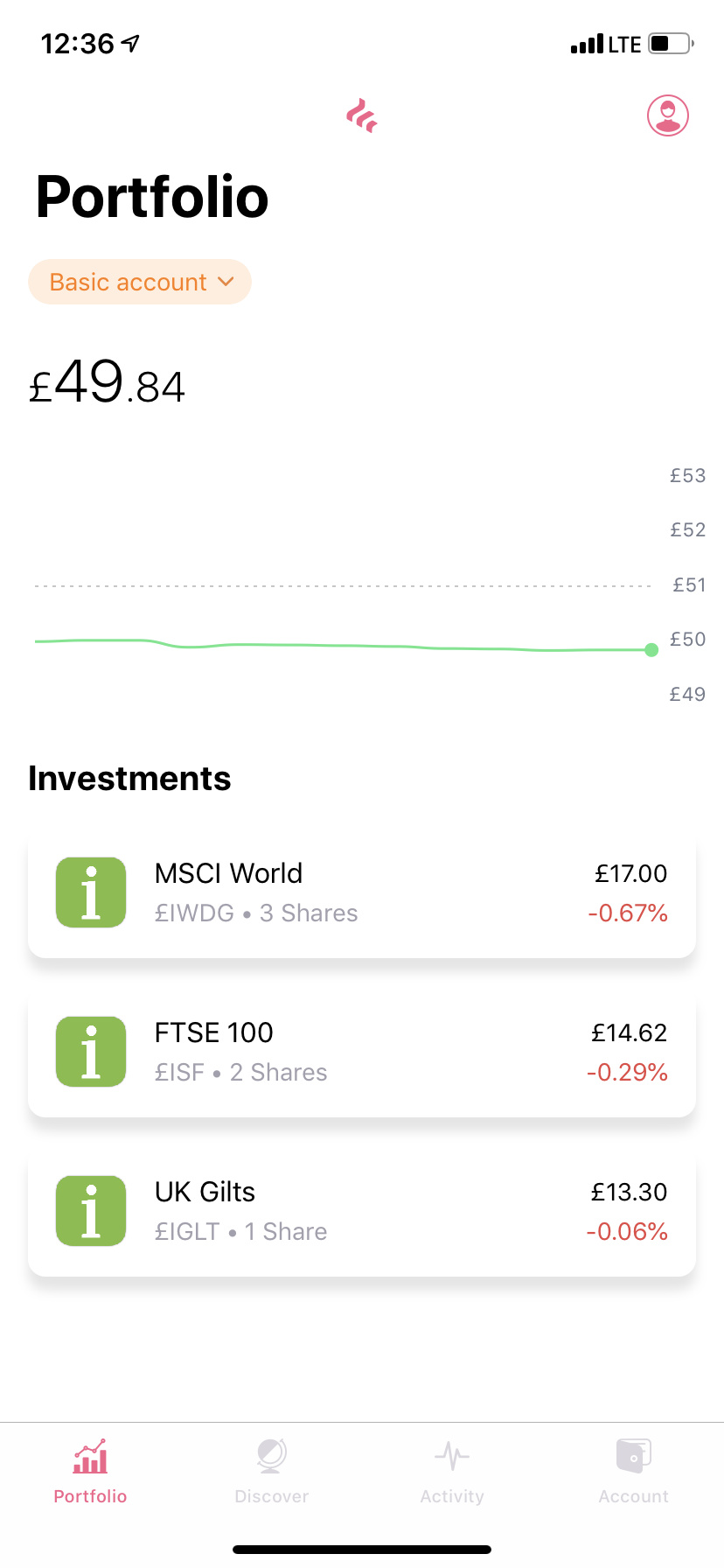

Dividends are payments sent out by the companies you have invested in. I’ve no idea what you have invested in using Moneybox, but let’s assume it’s some kind of broad fund comprising many different companies.

In that case, we might guess at a dividend rate of around 2%. This means if your current total investment value is £445, you will receive about £9 in dividends per year. Obviously it’s a long time before you exceed your dividend allowance. When you’re in danger of exceeding it, you’d want to move your investment to an ISA.

Your other consideration is capital gains. If you input £400 cash and your investment is now worth £445, and you choose to sell all £445, it means you gained £45. Your capital gains allowance per year is £12,000. If your gains are above that, you’d pay tax on the excess. So again, when you become in danger of your gains going over £12k, you’d want to switch to an ISA. For now just keep an eye on it every year, keeping in mind that you’re considering your cash inputs right from the very first year of investment vs current value, to work out your gains.

Don’t worry have a fish around on this forum with the search bar there is tonnes of information. This is an article from one of the freetrade team @Freetrade_Team that should answer some of your questions (and may lead to more, in which case ask!)

It’s weird that I mentioned here that it was 6 months ago that I joined the forum as I have literally just gotten my 1 year badge! Clearly I have been on here longer than I thought!

Moneybox’s standard charge seems to be £1/month + 0.45% of total, while Freetrade’s ISA accont charge is £3/month. 0.45% of £445 is £2, plus the £1 is £3. So if you have more than £445 already invested, Freetrade will be cheaper.

It’s 0.45% per year, charged monthly. So if your portfolio is £455 and stays static throughout the year, you’d pay £1 a month, plus 16p a month.

The breakeven point is around £5300, compared to FreeTrade, but that ignores the fund fees (0.12% - 0.30%) which matters, but is a far cry from the 8% in your calculations!

As an aside to the OPs question, can anyone recommend some good apps, news sources or forums to keep tabs on what people think the must-buy stocks are?

I have a decent enough understanding of the market and it’s mechanics and do my own research, but historically I invested in passives, and want to dabble a bit more with active stock selection.

There is no such thing I’m afraid, otherwise everyone would have been buying them.

The only single best solution is to buy a fraction of the entire market, which has always gone up historically. You can research ETFs like this yourself to find the best suited ones, but VWRL, for example, contains 2,900 holdings of all sorts. IWDG contains 1,641 different securities. Both are available via Freetrade and maybe could arguably with a grain of salt be considered relatively safe investments.

If you bought £100 in stocks of let’s say FTSE 100.

In the space of a couple months you dropped 20% of your value. You then have another £100 ready to invest, but you’ve just seen that you’ve lost £20 value.

Would a smart investor buy into that same stock at the lesser value, and simply wait and watch for the value to increase?

I can see the value in doing that, but surely there’s a limit of how low you would buy (or to know when to buy as you see it decrease in value) as you have the awareness that this is likely a dip and that it will return closer to the value you expect it to rise back to.

This would be the knowledge I lack entirely, if anyone could point me to some basics of watching stock value, understanding the common value of the stock and having the wisdom of knowing when the stock is likely just dipping, and when it’s likely over valued currently…

I know this is likely a “if we all knew then we’d all be millionaires…” kind of question but I’d like to learn what I can to know when’s a good time to buy a stock and when isn’t and perhaps holding off for a while

You can queue a basic trade when the market is closed but you can’t do an instant trade or queue one

Buying when it drops is a good move generally

Sudden drops can be due to political factors, a bad earnings report etc so there’s no magic solution to time the dip, but to understand the value of a stock you could read this

It depends on if you’re talking about stock of an individual company or a broad fund holding many companies. I think you’re talking about the latter since you mentioned FTSE 100.

If your fund is broad enough (eg. every stock in the world, instead of just the top 100 in the UK), you would probably gleefully buy more and more the further the stock market fell. I don’t think you’d worry about doing much analysis. This is because the whole reason you or anyone else invests in the stock market is that you have a belief that, over the long term, the stock market will rise in value. And sudden crashes are followed by sudden recoveries. And the ideal is to “buy low, sell high”. So buying stocks at an average cheap price will mean you can sell them later at an average high price.

If your fund is less broad, or you’re dealing with a single stock, then you have to look at the financials. Is the FTSE 100 down because of an irrational market panic, or because the UK government declared stock trading illegal? Is the company’s stock down because a large holder sold all their shares, or because they’re drowning in debt, have no way of generating enough profit to recover, and are on their way to bankruptcy?

In a nutshell you ask yourself “at these prices, what kind of future return can I expect?”. One simple rule of thumb is 1/PE (price to earnings ratio). You can find the PE of a single company, or consider the average of a whole country. The lower the price, the lower the PE, the more money you’ll make in the future, since the earnings are still there.

Thank you both for above, lots to think about and learn there. Will continue to read and learn.

Really stupid question time:

If you’ve bought just 1 share of a stock, at say £14, and the stock value/price nose dives to £0 (or below) - is that share lost/gone? Or do you still own the share that has no value (or minus value)? Or is this even possible…

It’s not possible for the value to be negative: that would mean you owe them money, which doesn’t make sense.

See the Debenhams - DEB.L thread for what can happen when a company goes bankrupt. But regardless of the specifics, if the company never makes money again (eg. because it ceases to exist), then your investment becomes more or less worthless because:

If you still had the ability to sell your shares, no one would want to buy them at any price

The company can no longer give you dividends

If the company’s assets are sold off, you still might not get any of that money because sale proceeds will cover loan debt first, and shareholders last

Already losing money but hey I clearly need to keep learning and looking for when the stock is in a low point with clear signs it is to rise in the long term; and investing my money at those moments.

With the free trades also being just once a day at the close of the market it seems, it puts more focus into per day value and looking at the value dips and highs over the longer term so I think it will actually help me learn as to know what day of the month to invest over say being concerned with daily/hourly ups and downs.

I’ve £50 coming from my moneybox in a few weeks which will be an additional investment alongside £50 a month. Just need to keep learning about finding the best day of the month to buy for one I’m eyeing up. I think for now I’ll just continue looking at ETFs until there’s at least a few hundred across them. I think others have said the first 1k/2k should be entirely ETFs though too.

If you need personal practical experience to learn this so be it, but make sure you learn the correct way: by keeping notes of every single time you guessed correctly, and wrongly.

What you will find is that, at best, you guess about 50% correctly. Most likely less than 50%.

But if you want to save yourself the time and hassle, I’ll give you the spoiler: it is not possible to time the market.

If there was an hour of the day that it was best to buy shares in, everyone would buy shares that hour… and then it would be the worst time to buy shares, since more buyers means higher prices.

If there was a day of the week, or a month, where shares were cheapest, then everyone would buy shares that day or month, and then it would become the worst day or month.

If you see prices dropping, you have a 50/50 chance of them either falling further, or bouncing back up. Chartists imagine that they can study the past performance, take various factors in to account, find patterns in the rises and falls, and predict “it’s going to go up now, not down”.

Academic studies have shown that chartists perform worse than random. They cannot predict the future. They do not know the best time to buy.

Neither do you, nor anyone else.

That’s really the key take-home point. Unless you have deep insider information that affects a very short term buy/sell decision, you have no edge over anyone else. They have the same information, and they almost certainly have access to it sooner than you, and can act on it orders of magnitude faster than you.

Buying a broad index tracking ETF is a situation where you honestly don’t even need to care what price you’re buying at. Over the long term, intra-day price fluctuations are meaningless. Even intra-year fluctuations will usually be meaningless. Even if you buy at the year’s highest price, you’ll still come out ahead over the long term.

The only way you come out poorly is you don’t invest at all (waiting for that “best moment” to invest).

Which is why the wise investors mantra is “time in the market beats timing the market”.

Anyway, you haven’t lost any money yet, and Freetrade’s free 4pm trade is just fine for you. If you learn one thing from this experience, it’s to ignore that % gains or losses. Just keep investing, and over a long enough time line you’ll come out ahead.

Good sir, you have been nothing but gracious with your time and patience afforded to me. I am truly grateful, if only everyone could have this fundamental education then investing wouldn’t be a scary thing for so many (millennial generations that saw bad things in stock markets destroying opportunity for them).

I will indeed continue to put my £50 aside a month at least. I am doing this for the long term, to just add money and let it do it’s thing and never touch it unless it’s to invest in something substantial far in the future like a home, a business, or maybe not until retirement comes around.

Start now, keep adding to it and don’t get cold feet. Sounds too simple, I love a hands off approach