Festicket are currently running a crowdfunding campaign via crowdcube for their

Series E. Freetrade have published some great material on recent crowdfunding campaigns, and I hope to emulate that. I’m an everyday private investor with no affiliation to Festicket beyond a pending investment; I’ve tried below to offer a balanced view on their campaign.

Festicket is an online music festival marketplace, offering all inclusive packages. Ultimately, the company mission is to streamline what is currently a convoluted booking process; consumers may book a festival experience encompassing travel, accommodation, merchandise, etc, under one platform. The website was founded by friends Zack, Jonathan and Jerome in 2013 following a frustrating experience organising a trip to Coachella.

The platform has become a 140-strong team, having catered to over 1Mn festival goers across 1.2K festivals, in 50 countries.![]()

![]()

![]()

![]()

Kicking The Tyres

The Team

Co-founder Zack Sabban has an academic background and some experience as an investment banker before founding festicket. He is apparently a festival fanatic, and currently holds the position of CEO.

Fellow Co-founder Jonathan Younes is a serial web entrepeneur, working in a founding member capacity at playlistnow.fm and ofcourse holding the position of CPO at Festicket.

The rest of the senior team draw experience from related firms in the industry, such as Ticketmaster, Eventbrite and SecretEscapes. The wider team seems to have modest diversity , with females in senior roles, which is great to see given the status quo 1. The 3 largest investors in Festicket also have staff sitting on the board.

Not bad.

Great emphasis is always placed on the team in startups, and for good reason. Execution risk is a big deal, and a great team heavily de-risks a startup. To put this into context: If the founder of GoCardless, having also worked for Starling Bank, had pitched his idea for an app-only challenger bank to me, I’d think most of us would’ve had (and indeed did have) a hard time holding on to our wallets. #Monzo

The Market

With the advent of piracy networks such as Napster, then digital streaming services such as spotify, music industry revenues have waned since the turn of the millenium. The likes of Spotify have boulstered growth, but sales remain a shell of their former glory.

“The death of rock was not a natural death. Rock did not die of old age. It was murdered.”

Gene Simmons, Esquire magazine

Perhaps because of this disruption, where music sales have stunted, the live music industry has boomed. Moreover,78% of millenials are turning toward spending on exeriences rather than material goods 2. Festicket’s model ultimately blends Ticketing marketplace with Online travel agency. Succes with the likes of Sofar Sounds bode well Festicket’s industry ![]()

The Live music market size is estimated at £19Bn. So a 5% global market share is what it will take to get that esteemed, yet elusive company status that’s all the rage. ![]()

The Business

Festival goers currently have to manoeuvre through a fragmented ecosystem; book travel here, accomodation there, then tickets over there. Festicket’s business proposition is to simplify this process into one or two clicks, under one platform.

Festicket’s main and perhaps only revenue stream is booking fees. This fee amounted to ~10% when booking for a day ticket at Download Festival, but this could be a fixed cost fee rather than a fixed percentage. This was similar to similar platforms, so a case has to be made to consumers that Festicket is superior to competitors. Customer acquisition cost isn’t mentioned, but this tends to be low for tech companies anyway.

Festicket have been backed by Beringea (A prominent VC known for backing AI startup “Threads Stylings” and salad bar chain “Tossed”). Festicket have also received investment from leading VCs such as Kima Ventures and Playfair capital. Not only do Venture Capitalists add value , but a well-funded startup with a large runway is substantially de-risked.

The company has some debt, the magnitude and nature of which is slated to be disclosed between campaign closure and capture of funds. Debt is the bane of Venture capital because:

- Creditors have priority of shareholders in the event of bankruptcy or similar, hurting returns.

- Funds could ultimately be used to pay off debt, rather than for growth, also hurting returns.

- Debt can sometimes convert to equity, thereby diluting shareholders and… hurting returns.

Valuation; The VC firm Edge investments is investing in this round (albeit on different terms, perhaps), and are said to have negotiated an undisclosed revenue multiple based on various ticketing and online travel agency deals. This qualifies the valuation in my view. There are many methods of valuation, such as the discounted cash flow method, (this suffers from a heavy reliance on forecasts) but revenue multiples are very much in vogue in venture capital.

Traction and Growth has been strong. Festicket was the 80th fastest growing company in Europe between 2014 and 2017 3. Company revenue grew 14 fold in this period, this amounts to a 140% CAGR. This establishes a product/market fit. Lack of market need is one of the most common reasons for a startup to fail 4, and is in part why pre-revenue startups are so much riskier than their revenue counterparts, or even scaleups. Festicket have accrued strategic partnerships with Eventbrite, Spotify, amongst others. Growth slowed in 2018, although the Company has pegged this down to their focus on senior recruitment at the time. This, coupled with a looming television marketing campaign, could position them for further growth.

The Competition

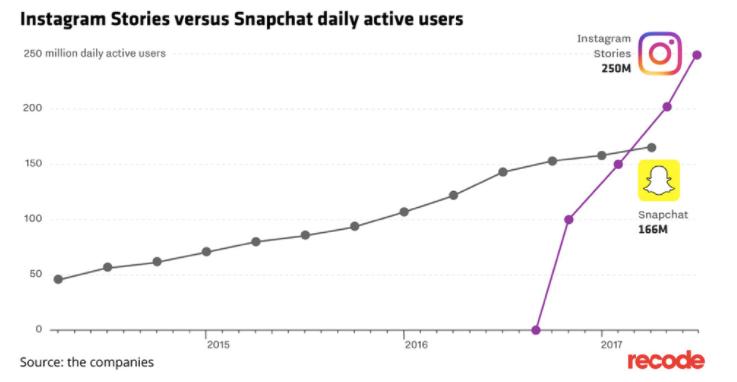

Festicket is de-risked in many ways. However, In my view, their is a very high risk of them being outcompeted. The startup seems to lack defensibility and there are very few barriers to entry in this space. Festicket have a notable first mover advantage, but little stands in the way of a copycat startup, or even larger, established platforms adopting Festicket’s model. My favourite example of this is how Instagram copied Snapchat’s ‘stories’ idea, and obliterated any hopes Snap might’ve had of increasing market share.

Festicket’s model is unique (for now), and they seem to be much larger than it’s rivals:

- Dice: Booking of festivals at face value, i.e. without booking fees. A very real threat imo, afterall, this is how Freetrade grew to prominence.

- Everfest: Effectively a booking platform and social network for festival experiences.

- Bandsintown: A platform that notifies and recommends users with nearby live music opportunities

- Ticket arena/Event Genius - An online ticket marketplace, with innovations including reserved seating mechanism and visualisation, Cashless POS, and so on.

The investment

Terms:

It’s not unheard of for one investor to make a healthy ROI, and another to make zilch, despite investing in the same company and round. Don’t underestimate the terms.

On offer are preference D shares (you get your share of any money, after preference A to C, but before E to Z, shareholders) which will be owned by Crowdcube Nominees Ltd, of which investors will be beneficial owners. The nominee structure has it’s pros and cons. Investors get voting rights, preferential rights to capital, but no pre-emption rights - This invites dilution (investors could end up owning a smaller slice of a bigger (or, in a downround, smaller!) pie.

Tax relief The shares are pegged to be EIS eligible 5. EIS scheme is a -quite possibly the best- tax relief scheme for investments offered in the UK.

EIS in a nutshell

Put simply: For every £10 invested, you get £3.00 as an income tax refund just for breathing. Should the company go bust, you get another £2.80 for your troubles 6. But tax risk is a thing, and there is no gaurantee that they will be successful applying for EIS relief after closing their funding round 7 . Moreso, if the they outgrow EIS relief eligibility or you sell the shares within 3 years, HMRC will ‘clawback’ the relief you claimed. But! Heed the adage: don’t let the tax tail wag the investment dog.

Exit strategies seem open, an IPO or M&A could be possible exit strategies; i’m leaning towards M&A. Possible acquiring companies inclue Eventbrite, given their size and recent activity. Festicket forecast a 6 fold increase in booking value by 2021. This amounts a return multiple of 6, or an IRR of 770% by my count. As always, I feel the forecast is optimistic.

Risks: Please see the disclaimer below for a quick summary of the risks. Startups and scaleups make for high risk, high reward investments. This can’t be stressed enough.

TL;DR

Festicket are a high growth VC backed startup offering an online marketplace for festival goers currently raising capital. They’ve grown fast, have a pool of talent, and some great partnerships. Perhaps because of a receruitment drive growth slowed recently, but a TV marketing campaign is looming. Furthermore, Festicket could very easily face stiff competition from startups with opposing models.

For those that would like to invest, have a look at their pitch deck, or ask their team some questions here is their crowdcube campaign page.

Would love to hear everybody’s thoughts on the campaign, good and bad; also, any criticisms of, or feedback on, my assessment are more than welcome. I will continue to edit/update the post and add references as needed.

{kind=link}

{kind=link}

{kind=link}

Disclaimer

N.B. This post does not constitute investment (nor tax) advice. I would however, like to stress that the mentioned investment opportunity exposes your capital to risk, notably dilution, lack of dividends, illiquidity and loss of capital. Where applicable, I encourage everyone to seek independant tax and/or financial advice. As for conflicts of interest, I have a pending investment in Festicket but no affiliation with the company beyond this.

Footnotes

1 Taken from the UK Government’s Female founders Report. 89% of VC investment goes to all-male founding teams. The same phenomenon is true of ethnic minorities. Equity finance seems to be moving towards a more democratic model, especially in the crowdfunding sphere; this ultimately leads to more exciting businesses emerging in my view.

2 Taken from Eventbrite. Eventbrite is now a partner of Festicket

3 The Financial Times list of the 1000 fastest growing companies in Europe

4 Chubby Brian Insights research on the top 20 reasons startups fail

5 It’s unusual for preference shares to get EIS relief. Normally, such shares don’t qualify because they don’t pose the same risk to capital as ordinary shares. Festicket’s investors include ‘venture capital trusts’, which must meet certain criteria similar to EIS; so this concern may be unfounded

6 This calculation assumes you are a higher rate tax payer. It works out at £3 tax refund to start, then a further £1.40 for your troubles should the company goes bust if you’re on basic rate.

7 Companies either get advanced assurance (Essentially a heads up from HMRC that the shares will get EIS relief. This heads up can be given before the paperwork is even submitted, thereby reassuring investors) during their fundraising campaign, or they simply apply for EIS relief after their campaign is complete