It looks like WeWork will be putting off going public for a little while longer..

Interesting timing - they seem to still have billions in cash in their balance sheet I don’t see why they needbyet another raise/infusion now.

Also interesting this is a direct investment, not from the vision fund - I’m not an expert on corporate structure but I think lots can be read into that - looks like they’re position share ownership for a potential IPO and to maximise return.

2 Likes

3 Likes

Is it just me or is that really bad?

5 Likes

Ethically it’s very bad. But the board cannot do much even if they wanted to because the CEO has majority voting rights. There’s a lot of startups with share structures like this.

2 Likes

Adam: “Hey WeWork, do you want to lease my building for a lot of money?”

[shuffles around so he’s facing the other way]

Adam: “Ooh yes please.”

[shakes hand with self]

Horrible ethically, but as @saf says there’s no effective governance. Facebook and others have similar structures.

3 Likes

Another excellent Polymatter video:

Complimentary Bloomberg coverage decent too:

2 Likes

WeWork appears to me to be one of the most overvalued companies in existence. I’ll be staying well away if/when they ever hit the public market.

2 Likes

A couple of bits of eye catching WeWork news -

& ![]()

3 Likes

This is really interesting, particularly with him taking money pre-IPO. The $700m isn’t all equity, loans backed against shares is bullish on the stock price, but either way this doesn’t fill investors with confidence I wouldn’t have thought!

My biggest issue here are the conflicts of interest; he has taken loans against stock previously, invested it in real estate, that WeWork then leases from him, meaning WeWork is paying him millions of $$ (also means revenue growth for WeWork > increases share price (he’s the largest shareholder) > maintains loans (that are probably paid for by the revenue he is generating from his lease of the building’s to his own company) > etc). All very circular and for the benefit of him, not the share price of the company.

The image of it being a money-making mechanism for him isn’t helped by the fact his wife is also employed in a very senior position.

These both demonstrate conflicts of interest, the first more than the second.

3 Likes

I am out of that one also. It looks like this year we have loads of overvalued IPO who are looking for cash injection. Interesting times

He couldn’t have sent worse signal before the IPO…

1 Like

Investor call 31 July.

WeWork is a “state of consciousness” (Neumann, 2018). He also owns property with a guitar-shaped room. Adam Neumann, CEO of WeWork, Owns Over $80 Million of Real Estate

“Reuters reported on Friday that WeWork, or rather its parent company We Company, plans to host an analysts’ day for Wall Street banks on July 31st, indicating that it wants to leave nothing to chance after other high-profile initial public offerings (IPOs) struggled or were scrapped this year, amid pushback from investors over eye-watering valuations sought.”

Once the S-1 form (IPO filing) is out next week, we can look at the financials and the shenanigans:

Adam Neumann describes what the We Company is doing as a “global physical platform.” But he’s been investing heavily in technology and has bought a succession of software startups in recent years. The company has also argued that it’s been and will generate valuable data about its clients over the years and how they use its space and that data could be offered as its own service or could form its own future products and services.

But many see We as just a real-estate company. Nearly all its revenue comes from memberships— essentially the rent payments made by its tenants. It’s also likely that most of its investments are going toward leases on properties and furnishings for those properties.

The answer to the question about whether its more a tech company or a real estate firm is important because it could have a direct bearing on its valuation — and how much public investors will pay for its stock.

Neumann dominates We. He has majority control of the company despite not having a majority economic interest in it, thanks to shares that give him extra voting power. Such arrangements have come under increasing scrutiny, because they’ve helped protect tech titans such as Facebook’s Mark Zuckerberg, Alphabet’s Larry Page, and Snap’s Evan Spiegel from being held accountable by investors or the public at large.

But even before his company has gone public, Neumann has given potential investors reason to worry about how he’ll exercise his power once it does.

He reportedly purchased buildings only to turn around and lease them to WeWork. Over the last five years, he’s raised $700 million by selling off his WeWork shares or using them to guarantee personal loans. And he and the company reportedly set up a new corporate structure recently that will allow him and other insiders to avoid paying taxes on any dividends We may pay out — while sticking other investors with double taxation.

Those moves are “red flags” for potential investors, said David Erickson, a senior fellow in finance at the University of Pennsylvania’s Wharton School of business.

2 Likes

‘Hard pass’ from me. Their central business model is not innovative at all - rent out large real estate in cities and retrofit it into a shared working space for small companies under the WeWork brand.

The whole idea behind the IPO is around the idea of We being a Tech company. I don’t buy it one bit. Their core business is fine but I’d guess that the IPO valuation will be substantially inflated on the basis of this idea behind the company being an innovative tech player.

We is essentially just a nicely packaged real estate company with a decent brand.

Avoid.

7 Likes

S-1 filed ![]()

Key takeaways:

- 528 co-working spaces in 111 cities across 29 countries

- 527,000 members

- WeWork has raised $8.4 billion in debt/equity since 2011

- $1.5 billion revenue in last six months

- With losses in the same period of $904.6 million

- May list as early as next month, with ticker $WE

The Acquired team are excited about it!

3 Likes

Interesting as well:

I did a quick scan of the Adam and Rebekah Neumann TV show script that is that pre-IPO S-1 filing: https://www.sec.gov/Archives/edgar/data/1533523/000119312519220499/d781982ds1.htm

And here’s my 20c - the co-founders are very rich:

Adam Neumann is like Mark Zuckerberg - you can’t do anything to him because:

Adam controls a majority of the Company’s voting power, principally as a result of his beneficial ownership of our high-vote stock.

He’s also the CEO and the Chairman.

? :

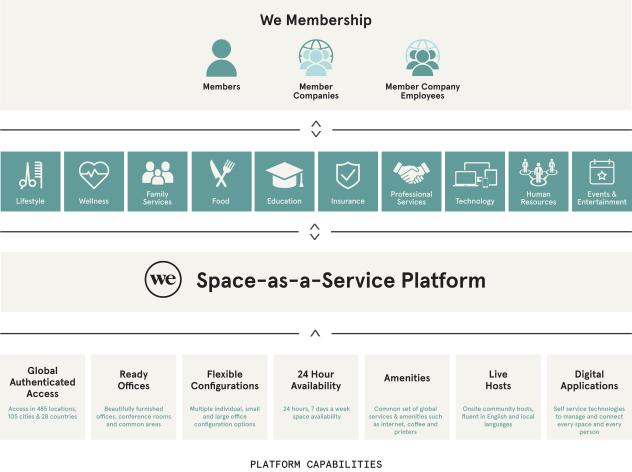

We pioneered a “space-as-a-service” membership model.

(No it didn’t. But at least it’s not pretending to be a tech company.)

Yes, they are a real-estate play:

Our strong unit economics, together with the increasing cost efficiency with which we open new locations, gives us the conviction to continue to invest in finding, building and filling locations in order to drive long-term value creation.

Management fees of some international arms - a bit like private equity management fees (chunky and straight to shareholders)… Also note that they could’ve invested in an image with a higher resolution but this could be deliberate, plenty of companies do this (“don’t look this way”) :

https://memeguy.com/photos/images/mrw-debt-collectors-call-216493.png

https://memeguy.com/photos/images/mrw-debt-collectors-call-216493.png

Expenses higher than revenue (but it’s only the income statement):

Related party transactions with Adam Neumann and ARK (which still channels money to Adam Neumann - see “Business—Our Organizational Structure—ARK”) in “Risk Factors”. Always read “Risk Factors”, which includes some honesty at least. Shady related party $ are always red flags, but a lot of people see no evil in that:

We have a history of losses and, especially if we continue to grow at an accelerated rate, we may be unable to achieve profitability at a company level (as determined in accordance with GAAP) for the foreseeable future.

We have engaged in transactions with related parties, and such transactions present possible conflicts of interest that could have an adverse effect on our business and results of operations.

We have entered into a number of transactions with related parties, including our significant stockholders, directors and executive officers and other employees. For example, we have entered into several transactions with our Co-Founder and Chief Executive Officer, Adam Neumann, including leases with landlord entities in which Adam has or had a significant ownership interest. We have similarly entered into leases with landlord entities in which other members of our board of directors have a significant ownership interest, such as through ARK (as defined in “Business—Our Organizational Structure—ARK”). See “Certain Relationships and Related Party Transactions”. We may in the future enter into additional transactions with entities in which members of our board of directors and other related parties hold ownership interests.

This is weird - also in “Risk Factors”:

Our future success depends in large part on the continued service of Adam Neumann, our Co-Founder and Chief Executive Officer, which cannot be ensured or guaranteed.

Adam Neumann, our Co-Founder and Chief Executive Officer, is critical to our operations. Adam has been key to setting our vision, strategic direction and execution priorities. We have no employment agreement in place with Adam, and there can be no assurance that Adam will continue to work for us or serve our interests in any capacity. If Adam does not continue to serve as our Chief Executive Officer, it could have a material adverse effect on our business.

New debt - $6bn in bank facilities - in addition to a whole lotta debt:

Risks Relating to Our Financial Condition

Our indebtedness and other obligations could adversely affect our financial condition and liquidity.

Concurrently with the closing of this offering, we expect to enter into a new senior secured credit facility (the “2019 Credit Facility”) providing for senior secured financing of up to $6.0 billion, consisting of a three-year letter of credit reimbursement facility (the “2019 Letter of Credit Facility”) in the aggregate amount of $2.0 billion and a delayed draw term loan facility (the “Delayed Draw Term Facility”) in the aggregate principal amount of up to $4.0 billion. …

…

In addition, we had existing consolidated long-term debt of $1,342.7 million as of June 30, 2019, including $669.0 million outstanding principal amount of our 7.875% senior notes due 2025 (the “senior notes”) and amounts under the 424 Fifth Venture Loans described in “Description of Indebtedness”, which loans are obligations of the 424 Fifth Venture but are recourse to us in certain limited circumstances.

Because of lease accounting, $1.3bn is just a portion of total debt :

Long-term leases are our primary means of securing real estate to deliver space-as-a-service to our members. We have early adopted ASC 842 in connection with the preparation of our financial statements as of and for the six months ended June 30, 2019. We applied the modified retrospective adoption method, and such financial statements reflect the adoption of ASC 842 as of January 1, 2019.

https://samanthafairjourney.files.wordpress.com/2018/10/1mletm.jpg

https://samanthafairjourney.files.wordpress.com/2018/10/1mletm.jpg

Because total debt - including leases and convertibles - is closer to $21.92 bn

Ok, this is still a real-estate company:

https://www.sec.gov/Archives/edgar/data/1533523/000119312519220499/g781982g62x27.jpg

https://www.sec.gov/Archives/edgar/data/1533523/000119312519220499/g781982g62x27.jpg

ARK was set up because of shady arrangements between Adam Neumann, the co-founder, and the company:

As a result, we are providing disclosure about all of these properties and, more importantly, have created a mechanism for an orderly transition of these properties from Adam’s ownership that ensures the Company gets a favorable treatment in the transfer of these assets. Adam has committed not to purchase any additional properties with the purpose of making them available for our occupancy.

Financial Times says it’s still paying to Adam Neumann:

and see this:

To stay afloat maybe they issued $1.7 billion in equity in 2017 and $1.8bn in debt in 2018:

which explains the “large” cash position at the end of December.

In 2019-2020 - more debt (at least $ 6bn of bank debt) and more equity issuance (this IPO).

One may argue that it’s using sensors, apps, etc - and therefore it’s a tech company - to justify the valuation.

![]()

{kind=link}

{kind=link}

{kind=link}

10 Likes

Together with Uber they are rapidly turning into the magic money disappearing machine.