Thanks for this @xnox I was looking at adding this one to build a dividend base but the drop has made me reconsider.

3 Likes

Don’t want to hijack this thread but this a reminder that these are not passive funds. They require careful due diligence and surveillance. Some are expensive and aggressively managed, others are not. Downing Renewables just announced a dividend raise today and has a low premium. Nextenergy solar has low debt and conservative power price assumptions.

3 Likes

That’s not a hijack, it’s a worthy comment PLUS I hadn’t heard of those two so I’ve gone and added my votes to the topics… though I’m not sure if FT take any notice of votes anymore.

I dumped TRIG after the ex-div date so I’ve dodged the recent decline which is very out of character for me. I normally ride things downward for a long time because I’m incompetent and possibly also a cow.

7 Likes

Nice! Now that you’re out I’m looking forward to seeing a steady increase over the next months ![]()

4 Likes

Why’s everyone so mean to me… ![]()

Freetrade moderators, help me, please, I’m being unfairly picked on!

3 Likes

Seeing this thread pop up again reminded me to share this blog post on the subject of renewable energy (the author is now a contributor to Monevator). Food for thought from May 2020.

Finumus - Don’t invest in Renewable Energy - May 2020

In relation to TRIG, the most interesting bit is the section on how renewable investments project NAVs are calculated:

"You raise some equity, borrow some money, lease some land, build a solar farm. You get a fixed, or inflation linked price for your power for some period (from 0 to 30 years) - i.e. a subsidy, or no subsidy thereafter you just get whatever the going-rate is. At some point your lease expires, and solar panels degrade by about 1% per year.

Most companies get a mix of fixed price for some term (i.e. subsidised) and the market rate, depending on when they built the farms. So some are more exposed to power prices than others, but all have a tail of cash-flows that are at ‘spot’ power prices.

Now, what are these things worth? We just take all the cash flows, the subsidised ones are like a weather-linked indexed government bond, and the no subsidy ones are just the future power prices. Then we discount those back to today using a discount rate, which is some, (picked out of the air) premium over the ‘risk-free’ government bond rate) - it’s business-school 101. The lower the rate, the more those in-the-future cash flows are worth.

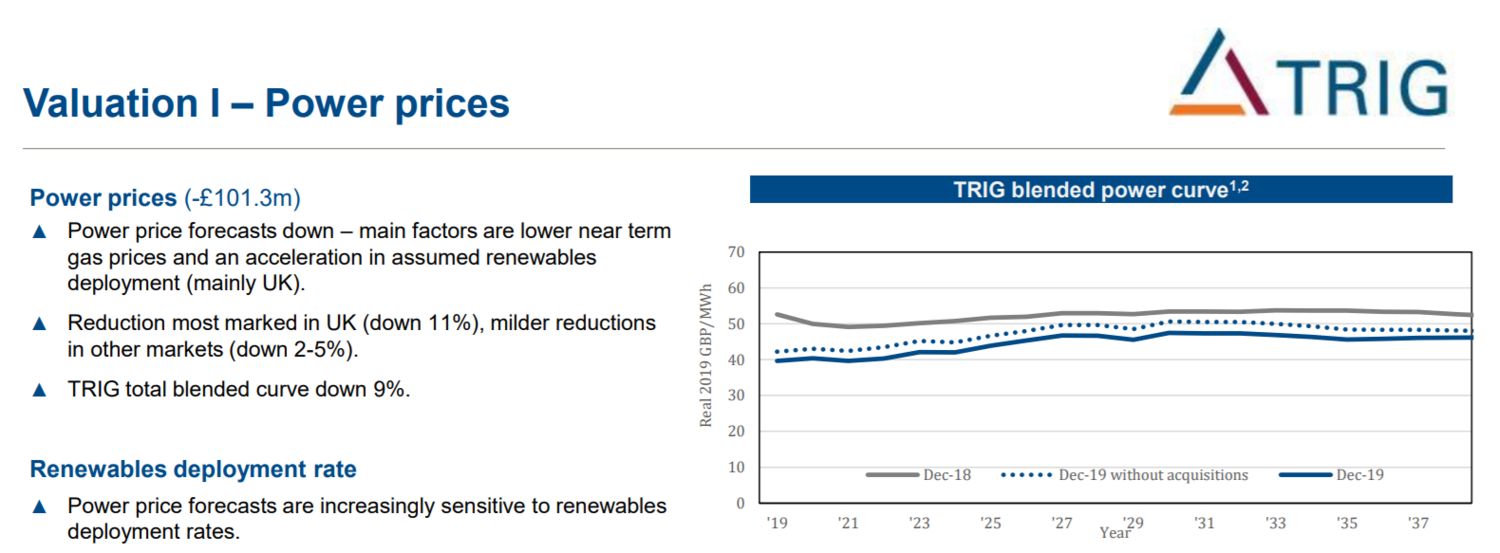

The Renewables Infrastructure Group (TRIG) has a very good chart on pages 10 of their 2019 FY results presentation, showing how this discounting works.

£101m write down. Not to worry, we’ll just reduce the discount rate, again. Source: TRIG 2019 FY Results presentation.

Then on page 11, they have the above delight, where they fus’up that they’ve been over-egging the pudding, and over-estimating future power prices. And are therefore going to take a £101m hit to the NAV. Now the problem is they are still being woefully optimistic. Their new 2040 power price assumption is about £44 per MWh, whereas Bloomberg New Energy Finance are estimating it’ll be £19 per MWh. £19 per MWh is about $0.016 per KWh, have a look at Ramez’s chart again - the UK’s a fairly high cost location, but it is windy - that looks doable. The conclusion is that these guys, and pretty much all the others, are over-estimating forward power prices by more than double . I’m not picking on TRIG here, I’ve actually got a lot of time for those guys. I choose them at random, knowing what I’d find.

They’re all at it

And here’s the fundamental problem: they all have to do this. There’s tonnes of money looking to invest in these sorts of projects, and the way to get the capital is to be optimistic about forward power prices in pitches to your investors, so that you can secure the financing. The entire industry is cannibalizing itself. This is going to be just like Victorian railroads, there’s going to be massive infrastructure investments, those are going to fundamentally change society for the better, and nobody’s going to make a dime. There’s a great article about the specific impact on the UK renewables trusts, here."

5 Likes

interim results 2021")

2 Likes

Yep really good. That’s why I looked at each funds fixed-price exposure to determine risk. I’d jot down the date for each one (e.g majority fixed price until 2033) and maybe some details on how diversified or not it was and use that to compare or even monitor ones I’d invested in. You can find contract details in almost every earnings release, say TRIG’s H1:

Usually its a graph of some sort with “contract” or “revenue split” mentioned. Its on page 20, and just googling all the different types of contract type gives you an idea of what is fixed/subsidy and what is market. In this case TRIG will be predominantly selling to market by 2034, and this may increase over time. So then you need to check what management’s expectations are for prices, you can find TRIGs power curve on page 38. As we can see from the above, their assumptions for future power prices have reduced from over £50/MWh to less than £30/MWh over the last 3 years. This affects NAV and ultimately dividend policy.

Addendum: TRIG have actually taken the hard part out of this by providing the pie charts on page 15. Keep in mind however that future fixed revenue here is as determined by management, and therefore fixed revenue % may not be achievable.

Closer to the 2030s, when it will get harder to get long-term arrangements at similar prices and subsidies wane it’ll be all about each fund manager’s price forecasts (including whether they have switched to CPIH as pointed out in the linked article) and their respective effect on NAV.

6 Likes

That is very interesting now ![]() thanks xnox

thanks xnox

2 Likes

I understand that this is a self investment platform. But I wonder if Freetrade does any minimum screening and remove stocks from ability to buy if/when they deteriorate.

I guess that’s a completely different can of worms.

Gas prices are going up recent which should be bullish for renewables. But prices are fixed ahead of time hence actual correlation with other energy sources is not there.

1 Like

“Your capital is a risk”

One mans deteriorating stock is anothers buying opportunity. $RIDE & £AMGO are two that should have hit the dirty already but somehow limp on.

6 Likes

Looks like TRIG is now at £1.24 to buy direct. Thus rights issue is no longer at a discount.

2 Likes

What does that mean sorry direct and discount? ![]()

1 Like

Think he’s saying the current price has dropped to the same as the price in the rights issue earlier this year

I guess if you bought in the rights issue you could have sold for a profit between then and now though

Edit: I see now he meant the primary bid issue. I thought he meant the rights issue back in march. so I guess there hasn’t been chance to get out at a profit

2 Likes

It’s about the article I posted 10 days ago if you want more details:+1: I got an email from primary bid to buy at that price last week sio assume many others did.

3 Likes

I was referring to the Primary Bid offer of new shares that at the time it was announced was at a discount. Since that announcement the share price has dropped down to the same level as Primary Bid. Thus there is little benefit of doing purchase via Primary Bid.

(It can’t deposit shares to Freetrade, so will need to go to some other broker, which might be cheaper if said other broker charges high fees and the trade size is large. Hence majority of Freetrade users can ignore Primary Bud offer).

3 Likes

Bumping this thread rather starting anew. I would be interested in what people think about the potential of TRIG while energy prices are on the up?

I’ve got a small holding but plan to increase it over the coming months. I was wondering if the value of these shares is likely to rise as income from the facilities increases due to increased cost of electricity? At some point I wonder if the growth of this company will become an issue too, for the same reason. Production of facilities, particularly wind power which requires a lot of energy dense concrete will become very expensive.

What are your positions on TRIG?

1 Like

Long term hold for me (as part of my dividend income portfolio). Topped up March last year.

2 Likes

High power prices now doesn’t necessarily mean bigger profits for renewables operators. Many lock in power prices 2 years in advance to protect against down side risk, and therefore miss out on upside. I haven’t looked into detail at TRIG power price hedging - but just thought I’d flag.

In any case, I think the market would have likely priced in any upside from higher power prices.

Thank you @Bombastic_Bear I had not thought of that. They are invested in 79 projects, so maybe some will come up for renewal soon.

Can you explain to me how the market would price in any upside from higher power prices please? I have so much to learn!

1 Like